I have been actively developing real estate for ten years, and, through my law and consulting practices, have advised real estate developers for almost three decades. So, when I say that we’re living through the most challenging commercial real estate development environment of my career, I offer that with some perspective and context.

And the challenges are manyfold. The cost of real estate capital has not been higher for generations. And the cost to operate a Western New York (WNY) apartment project has nearly doubled since the start of the COVID-19 pandemic, far outpacing income and rent growth during that same period. The cost of construction (both labor and materials) has never been higher in WNY on a per square foot basis, and tariffs on construction materials sourced from places like Canada and China will only exacerbate matters.

So what, then, are commercial developers facing these headwinds to do, exactly? Some are treading water and tidying their houses, praying for the good ol’ financeable days to return. Others, who either see those days in the rearview mirror, or who simply are pot-committed, are pressing forward with riskier deals featuring more personal investment and taller capital stacks. In any case, these are not times (or deals) for the faint of heart.

I suppose it should not be surprising, then, that public economic development incentives are at a premium these days. Low-hanging fruit, such as industrial development agency incentives and as-of-right property tax and utility abatements, long have been placeholders in experienced local developers’ budgets. These days, harder to reach incentives, such as commercial tax credits, also are shifting from optional to imperative. And deals that may have worked with a “stand-alone” tax credit prior to the COVID-19 pandemic now require multiple layers of tax credits just to pencil-out.

Enter New York’s brownfield redevelopment tax credit (BTC). As detailed in Part 1 of this series, New York began offering tax credits to developers for cleaning up and redeveloping brownfields in 2003. Since then, over 500 such projects have been undertaken across the state, and the program has become so popular with developers that New York legislators recently introduced a beefy $50,000 application fee and new “gates” for the admission of New York City projects, in part to manage project flow and optimize the program’s budget.

New York’s brownfield cleanup program (BCP) is popular with developers for good reason. It’s a fairly deep subsidy, considering there is no federal counterpart program, as there is with tax credits for affordable housing and historic preservation. It’s also relatively easy to monetize, given the program’s refundability feature and lack of an extended regulatory period. There’s also a fast-growing market for the “syndication” (essentially, trading) of BTCs to third-party investors seeking tax shelters. What’s more, BTCs pair well with other tax credits and incentives, allowing them to be slipped into financings beneficially and without much transactional disruption.

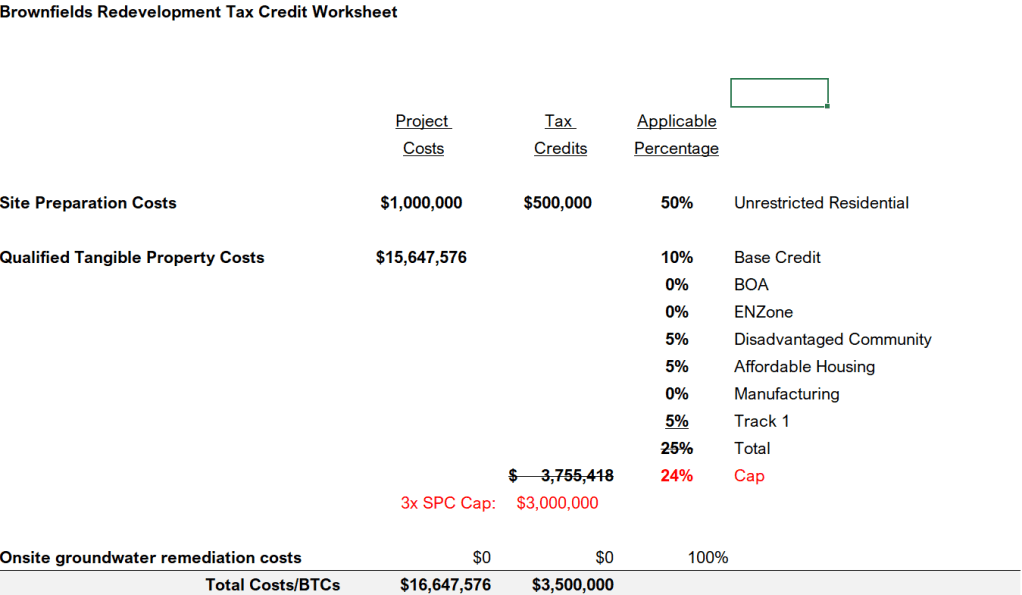

Here’s how the BTC program helps finance real estate development projects. When a developer of an approved BCP project completes the remediation portion of their scope, New York awards a tax credit based on the cost of that “site preparation”. The amount of that site preparation tax credit ranges from 22% to 50% of eligible costs, depending on the level of cleanup undertaken. That site preparation tax credit is available for the tax year that the project receives its certificate of completion from DEC.

When the developer completes the redevelopment portion of their project (generally evidenced by a certificate of occupancy), New York awards a “tangible property” tax credit based on the eligible costs that are part of the total development cost of the project.

The amount of a project’s site preparation cost is a factor when calculating a project’s tangible property tax credit: for non-manufacturing projects, such credits are capped at three times the project’s site preparation cost, while credits for manufacturing are capped at six times that amount. Early generations of the BCP did not include such a cap, leading to some liquidity issues stemming from massive downstate redevelopment projects.

A project’s tangible property tax credit is calculated based on a number of factors, including the level of cleanup, the location of the project, and the project’s end-use(s). The base tangible property tax credit currently is 10%, and the maximum credit allowed is 24%.

Here are sample calculations of the site preparation and tangible property tax credits generated by a WNY adaptive reuse project:

A few additional notes about BTCs:

- As illustrated above, even when capped, the BTC is designed to cover the full cost of the cleanup, as well as a portion of the redevelopment cost.

- Refunds of New York BTCs are federally taxable, so developers should plan and reserve for that event.

- Projects offering enough tax credits to justify the cost of syndication can expect to raise as much as $.80+ per one dollar of BTC, depending on the project’s size and structure, the wherewithal of the developer, and the nature of the investor for the BTCs.

- Because BTCs are awarded after cleanup and redevelopment, and after a sometimes-lengthy tax audit, some developers seek “bridge” financing to help pay project costs while they await a refund or an investment infusion. The repayment of BTC bridge loans generally are secured by a lien on the proceeds from the monetization of the BTCs, as well as by the personal guaranties of project sponsors and/or backers.

- It is highly recommended that first-time BCP developers seek legal and accounting guidance from professionals with BCP/BTC experience.

_________

Jason Yots has been a real estate and tax credit development attorney since 1996, and currently is a partner at the law firm of http://www.chwattys.com. Jason also is a founder of http://www.preservationstudios.com, an historic preservation consulting firm, and http://www.commonbondrealestate.com, an historic rehabilitation firm. He is based in Buffalo, NY.

Leave a comment